Free-space optics seen as viable alternative to cable

When communications managers face wireline deployment issues and compare the cost of a leased telecommunications line to the implementation of a free-space optics (FSO) system, the flexibility of the FSO products proves to be an attractive alternative. FSO communication links consist of optical data and voice transmission systems utilizing lasers to transmit digital signals through air instead of optical fiber. Major market drivers for this technology include the need for faster deployments, last mile solutions, and secure wireless links. The trend in FSO systems is to support longer distances (up to 5 km) and faster data rates such as 10 Gbits/sec.

When cost and other obstacles stall deployment of fiber-optic cables, the product and deployment opportunities for FSO systems improves. Communications managers are willing to consider FSO as the primary—and permanent—solution for bringing high-bandwidth capabilities to their premises.

But what about radio frequency/microwave wireless? Can optical wireless compete with these technologies—and take market share? FSO vendors claim that optical wireless accommodates secure transmission links at higher data rates over a system that does not require spectrum licensing, unlike RF/microwave wireless. Moreover, FSO vendors are addressing concerns regarding beam security, eye safety, licensing, atmospheric-condition problems, and line of sight issues such as a flock of birds interfering with the link performance. (More than 30 companies are supplying FSO communications systems worldwide.) As data rates reach multigigabits per second and optical communication increases, vendors' emphasis on low-cost, quickly deployed systems is encouraging to FSO prospects.

Optical wireless technology is prevalent in military applications. The U.S. Army is aggressively upgrading 400 of its facilities with FSO systems that can support Gigabit Ethernet (GbE) data rates. Its I3MP program is spending $50 million annually to replace landline links with FSO. Similarly, the U.S. Air Force's NetCents program is in the process of spending $75 million a year on FSO, upgrading all Air Force bases worldwide with GbE.

FSO systems are finding their way into non-military applications as well. Point-to-point and line of sight applications such as building-to-building installations serving the 50–5,000-m link length can be activated rapidly. The FSO systems can operate at rates up to 10 Gbits/sec; therefore, this technology is well positioned to compete against the high cost of cable deployment and rights-of-way issues.

Telecom carriers are also making some noise about FSO. In February, AT&T chairman and chief executive David Dorman stated his company's interest in FSO: "We're providing customers a clear path to a fully integrated, converged, and applications-driven future. We're also developing a range of alternate access strategies for AT&T, using wireline, wireless, and free-space optics technologies, to position us to bypass the Bell stranglehold on the last mile and reduce our largest corporate expense."

Fiber-optic cable is difficult to deploy quickly and economically—especially in downtown areas. To minimize risk, carriers are targeting fiber-cable deployment at new greenfields or high-density tall shiny buildings. RF and microwave can fill the gap, but these technologies have licensing, interference, and capacity issues.

FSO-link systems are typically segmented into two categories depending on the operating wavelength: 780–850 nm and near the1550-nm band. Major reasons for selecting 1550-nm FSO systems include laser eye safety, reduced solar background radiation, and compatibility with existing technology infrastructure. According to vendor fSONA Communications (Richmond, British Columbia), carrier class FSO systems must be designed to accommodate heavy atmospheric attenuation, particularly fog. Although longer wavelengths are favored in haze and light fog, under other conditions of very low visibility, this long-wavelength advantage does not apply. However, the fact that 1550-nm based systems are allowed to transmit up to 50 times more eye-safe power will translate into superior penetration of fog or any other atmospheric attenuator.

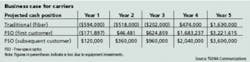

Data provided by fSONA shows FSO systems becoming attractive when the return on investment of the technology is evaluated against a fiber-based solution. The data in the Table is based on the following assumptions: five buildings, 50 customers per building, $24,000 average revenue per customer per year, $100,000 for connectivity, $10,000 in fiber equipment (DWDM), $30,000 in FSO equipment, 10% customer penetration the first year, 15% the second year, and 20% the third year.

In just 14 months, the entire FSO telecom-carrier network has paid for itself. Given the same assumptions, it takes almost four years for the fiber build to pay for itself.

Fiber-optic-component manufacturers should evaluate the potential FSO market, if they haven't already. Lightconnect (Newark, CA) recently announced an ultra-fast multimode variable optical attenuator (VOA) for FSO systems. The VOA has a typical response time of 30 µsec for scintillation compensation. According to the company, one of the major challenges facing FSO communications systems is scintillation or atmospheric turbulence. These fluctuations in the amplitude of the received signals are very rapid. ..